82% of small businesses that fail cite cash flow problems as the primary cause. Not bad products, not lack of customers – cash flow. The business was viable, but the money didn’t arrive when it needed to.

Understanding the most common cash flow problems is the first step to preventing them.

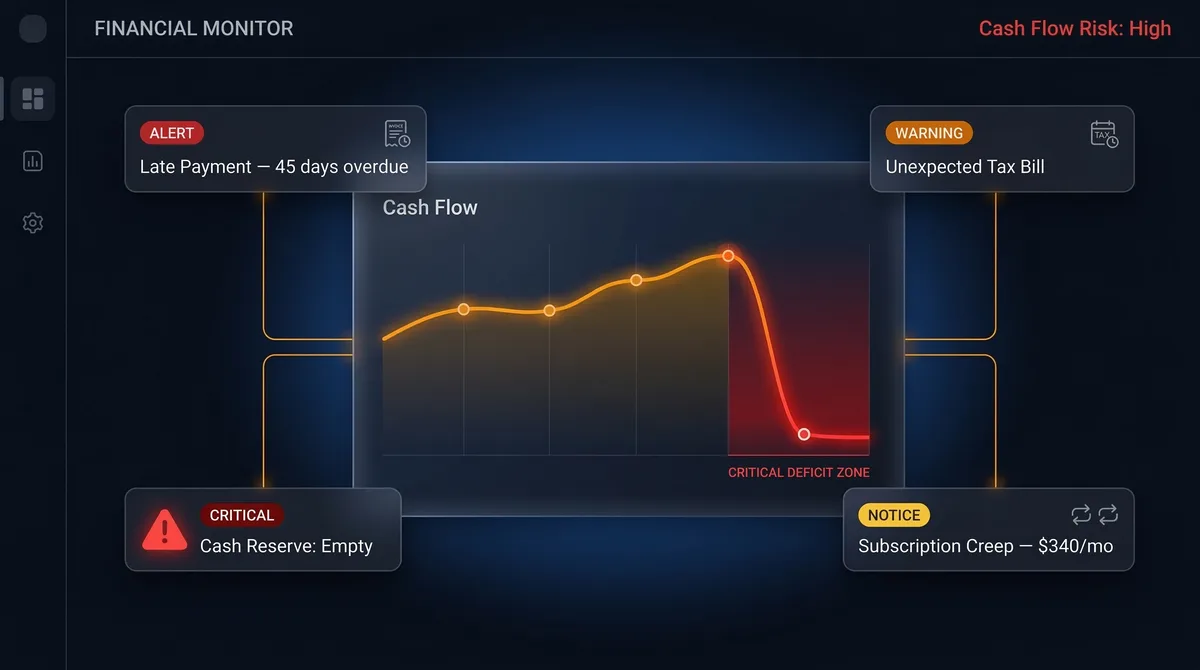

The 7 Most Common Cash Flow Problems

1. Late-Paying Clients

The average small business has $17,500 in outstanding unpaid invoices at any given time. One in four freelancers reports waiting over a year to get paid. Late payments are the single biggest cash flow killer.

Fix:

- Set clear payment terms before starting work

- Invoice immediately upon delivery

- Send reminders at 7, 14, and 30 days overdue

- Require deposits for new clients and large projects

- Consider late payment fees (1.5% monthly is standard)

2. Seasonal Revenue Swings

Many businesses experience dramatic income fluctuations – accountants are slammed January through April but quiet in summer, landscapers peak in spring and fall, consultants see slowdowns in December. The problem isn’t the swing itself – it’s failing to plan for it.

Fix:

- Analyze your revenue by month for the past 2-3 years to identify patterns

- Build reserves during peak months to cover slow periods

- Reduce discretionary spending in historically slow months

- Develop off-season revenue streams where possible

3. Invisible Expenses

Small recurring charges, forgotten subscriptions, and uncategorized spending create cash leaks that are individually minor but collectively devastating. A freelancer with just 5 unnecessary $30/month subscriptions is losing $1,800/year – enough to cover a month of operating expenses.

Fix:

- Track every expense – use an AI receipt scanner to capture purchases automatically

- Review categorized expenses monthly to spot patterns and waste

- Upload bank statements to catch expenses you might have missed

- Cancel or downgrade anything you haven’t actively used in 30 days

4. Underpricing

Many freelancers and small businesses set prices too low, leaving insufficient margin to cover expenses and build reserves. Revenue looks fine, but after expenses there’s nothing left for cash reserves or growth.

Fix:

- Calculate your true cost of doing business (including taxes, insurance, retirement, equipment, and unpaid time between projects)

- Price for profit margin, not just market rate

- Raise rates annually – even 5-10% compounds significantly

- Track your actual expenses to know your real break-even point

5. No Cash Reserve

Without a buffer, any disruption – a late payment, an unexpected expense, a slow month – creates an immediate crisis. You’re one bad week away from missing bills.

Fix:

- Target 3 months of operating expenses as a minimum reserve

- Set aside 10-15% of every payment received until you reach the target

- Keep reserves in a separate account you don’t touch for daily operations

- Replenish immediately after any withdrawal

6. Tax Surprises

Self-employed individuals owe both income tax and self-employment tax (15.3%). A freelancer earning $100,000 in profit might owe $30,000+ in taxes. If that cash wasn’t set aside quarterly, the annual tax bill is a cash flow catastrophe.

Fix:

- Set aside 25-30% of every payment in a dedicated tax account

- Pay quarterly estimated taxes on time (April 15, June 15, September 15, January 15)

- Track all deductible expenses to reduce your tax burden – SparkReceipt catches deductions you’d otherwise miss

- Work with an accountant before tax season, not during it

7. Growing Too Fast

Counterintuitive but common: rapid growth kills cash flow. You hire before revenue scales. You invest in capacity before clients pay. You take on bigger projects that require more upfront spending. Revenue is up, but cash is down.

Fix:

- Fund growth from cash flow, not credit

- Hire or invest only after cash (not revenue) supports it

- Require larger deposits on bigger projects

- Grow incrementally rather than all at once

Warning Signs Your Cash Flow Is in Trouble

Catch these early before they become crises:

- Checking your bank balance anxiously before paying bills

- Using credit cards to cover operating expenses

- Delaying payments to vendors or contractors

- Dipping into tax reserves for operating costs

- Declining work because you can’t afford the upfront costs

- Not knowing exactly what you spent last month

The Cash Flow Recovery Plan

If you’re already in a cash flow crunch:

- Get visibility immediately – Scan every receipt, upload bank statements, and categorize all expenses. You need to see the full picture.

- Collect what you’re owed – Send reminders on every outstanding invoice today.

- Cut non-essential expenses – Pause anything that doesn’t directly generate revenue.

- Negotiate payment plans – If you owe money to vendors, most prefer a payment plan over non-payment.

- Prevent recurrence – Set up automatic expense tracking, build a cash reserve, and do monthly cash flow reviews.

Key Takeaways

- 82% of business failures trace back to cash flow – it’s the #1 business killer

- Late payments, invisible expenses, and tax surprises are the most common culprits

- The first step to fixing cash flow is knowing what you spend – track every expense automatically

- Build a 3-month cash reserve to absorb disruptions

- Do monthly reviews to catch problems before they become crises

Related reading: Cash Flow Management for Freelancers and Small Business: The Complete Guide

Try SparkReceipt free

AI-powered receipt scanner and expense tracker for small business.

Get started