Self-Employment Tax Calculator

Calculate your Social Security + Medicare tax as a freelancer or 1099 contractor.

Estimates only. SE tax applies to net self-employment earnings of $400 or more. Consult a tax professional for your specific situation.

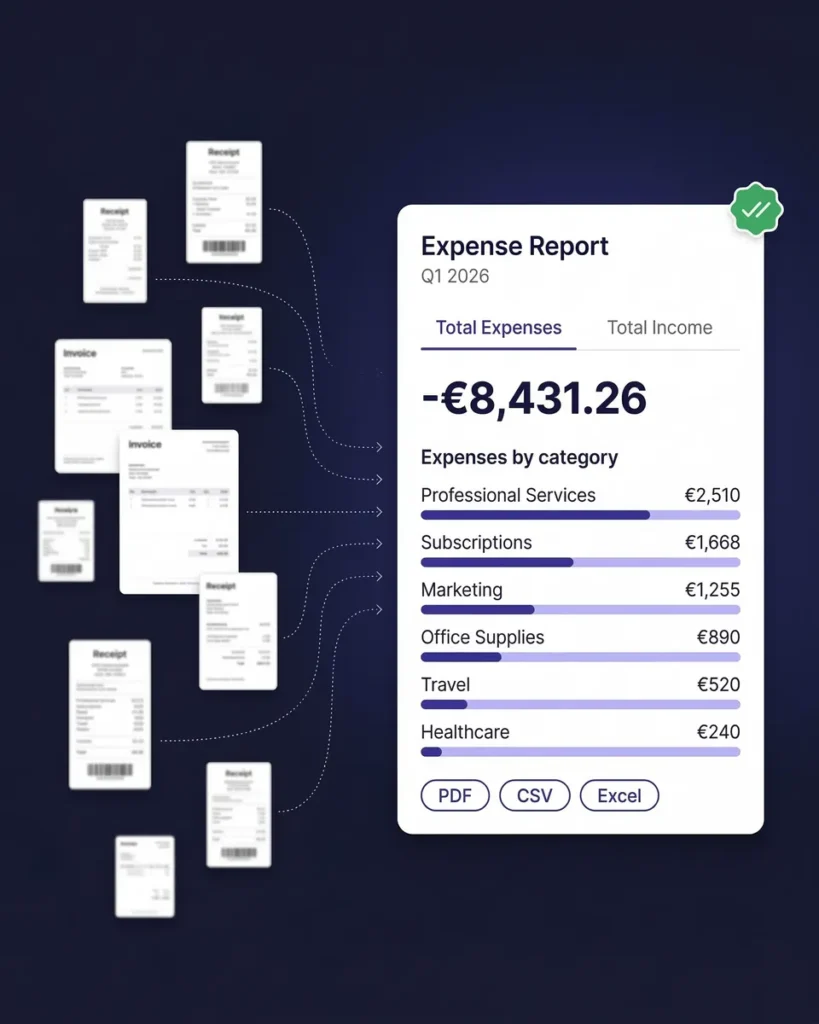

Track your expenses to lower SE tax

Every business expense reduces your net SE income—and your self-employment tax. SparkReceipt auto-captures receipts and categorizes expenses.

Start 7-day free trialHow Self-Employment Tax Works

Social Security + Medicare for the self-employed

Self-employment tax is how freelancers, independent contractors, and sole proprietors pay into Social Security and Medicare. When you’re employed by a company, your employer pays half of these taxes and you pay the other half. When you’re self-employed, you pay both halves — a combined 15.3%.

The SE tax breaks down as:

- Social Security: 12.4% on net earnings up to the wage base cap ($176,100 in 2025, $178,200 projected for 2026)

- Medicare: 2.9% on all net earnings — no cap

- Additional Medicare: 0.9% on earnings above $200,000 (single) or $250,000 (married filing jointly)

The IRS doesn’t tax your full net income — you first multiply by 92.35% to simulate the employer-half adjustment that W-2 workers get. Then you can deduct 50% of your SE tax on your Form 1040, reducing your adjusted gross income.

SE tax applies to anyone with net self-employment earnings of $400 or more. You calculate it on Schedule SE and file it with your annual tax return.

How to Reduce Your Self-Employment Tax

Strategies to lower what you owe

Unlike income tax, there are no brackets or standard deductions for SE tax — it hits every dollar of net earnings. But you can lower the amount you owe:

1. Deduct every legitimate business expense

Every dollar of business expenses reduces your Schedule C net income, which directly reduces your SE tax. Common deductions self-employed workers miss:

- Mileage deduction — 72.5¢/mile in 2026

- Home office deduction — simplified or actual expense method

- Health insurance premiums (100% deductible for self-employed)

- Software, subscriptions, and tools

- Professional development and courses

2. Maximize retirement contributions

SEP-IRA contributions (up to 25% of net SE income, max $69,000 in 2025) and Solo 401(k) contributions reduce your taxable income. While these don’t directly reduce SE tax, they lower your income tax significantly.

3. Consider S-Corp election

If your net SE income exceeds roughly $60,000, electing S-Corp status can save thousands. You pay yourself a “reasonable salary” (subject to FICA taxes) and take the remainder as distributions (not subject to SE tax). Consult a tax professional for your specific situation.

Start by tracking every expense with SparkReceipt — the average self-employed user finds $3,000–$5,000 in missed deductions, saving $460–$765 in SE tax alone.

Quarterly Estimated Tax Payments

Pay-as-you-go deadlines and safe harbor rules

Self-employment tax is pay-as-you-go. The IRS expects you to make quarterly estimated payments throughout the year — not one lump sum in April. If you owe more than $1,000 at filing time, you may face an underpayment penalty.

2026 quarterly deadlines:

| Quarter | Period Covered | Due Date |

|---|---|---|

| Q1 | Jan 1 – Mar 31 | April 15, 2026 |

| Q2 | Apr 1 – May 31 | June 15, 2026 |

| Q3 | Jun 1 – Aug 31 | September 15, 2026 |

| Q4 | Sep 1 – Dec 31 | January 15, 2027 |

Safe harbor rules to avoid the underpayment penalty:

- Pay at least 100% of last year’s total tax liability through estimated payments, OR

- Pay at least 90% of this year’s tax liability

- If your AGI was over $150,000 last year, the safe harbor threshold is 110% of last year’s tax

Use Form 1040-ES to calculate and submit your quarterly payments. You can pay online at IRS.gov/payments, by mail, or through the IRS2Go app.

Self-Employment Tax FAQ

What is the self-employment tax rate for 2026?

The self-employment tax rate for 2026 is 15.3%, the same as 2025. This consists of 12.4% for Social Security (on earnings up to the $178,200 wage base cap) and 2.9% for Medicare (on all earnings). An additional 0.9% Medicare tax applies to earnings above $200,000 for single filers or $250,000 for married filing jointly.

Who has to pay self-employment tax?

Anyone with net self-employment earnings of $400 or more per year must pay self-employment tax. This includes freelancers, independent contractors (1099 workers), sole proprietors, gig workers (Uber, DoorDash, etc.), and general partners. S-Corp owners pay FICA on their salary but not on distributions.

Can I deduct self-employment tax?

Yes — you can deduct 50% of your self-employment tax as an adjustment to income on Form 1040 (line 15). This deduction reduces your adjusted gross income (AGI) and your income tax, but it does not reduce your SE tax itself. It’s the IRS’s way of treating you similarly to how employers and employees split FICA taxes.

How do I calculate quarterly estimated tax payments?

Estimate your total annual SE tax and income tax, subtract any withholding from other sources (like a W-2 job), and divide the remainder by 4. Pay each quarter by the deadline (April 15, June 15, September 15, January 15). If your income is irregular, you can use the annualized income installment method on Form 2210 to adjust payments by quarter.

Does self-employment tax include income tax?

No. Self-employment tax and income tax are separate obligations. SE tax (15.3%) funds Social Security and Medicare. Federal income tax (10%–37%) funds general government operations. When self-employed, you owe both — which is why your total effective tax rate can feel high. Your quarterly estimated payments should cover both.

How can I lower my self-employment tax?

Reduce your net self-employment income by claiming all legitimate business deductions — mileage, home office, health insurance, supplies, software, and professional services. For higher earners ($60K+ net), S-Corp election can save thousands by splitting income between salary and distributions. Maximizing retirement contributions (SEP-IRA, Solo 401k) reduces income tax but not SE tax directly.